Tree Service & Arborist Insurance

Specialty insurance for tree trimmers, arborists, climbers, stump grinders, storm-cleanup crews, utility line clearance contractors, and forestry operations. Built around how tree work actually gets done — climb, cut, rig, drop, grind, haul.

The Specialty Insurance Hub for Tree & Arborist Operations

Tree work is a high-severity class that the standard small-business insurance market regularly declines. A single misdirected limb can total a roof, a vehicle, or a fence run. A climbing fall can become a six-figure workers compensation claim. A subcontractor without proper coverage can become your loss.

Kelly Insurance Group places tree service and arborist accounts every day. This hub connects the full library of tree-specific coverages, operations-specific pages, cost and quote resources, and hard-to-place placement options — including accounts with prior claims, cancellations, declinations, crane operations, and utility line clearance work.

If you climb, cut, rig, drop wood, grind stumps, haul debris, or run a forestry crew — this is the right starting point.

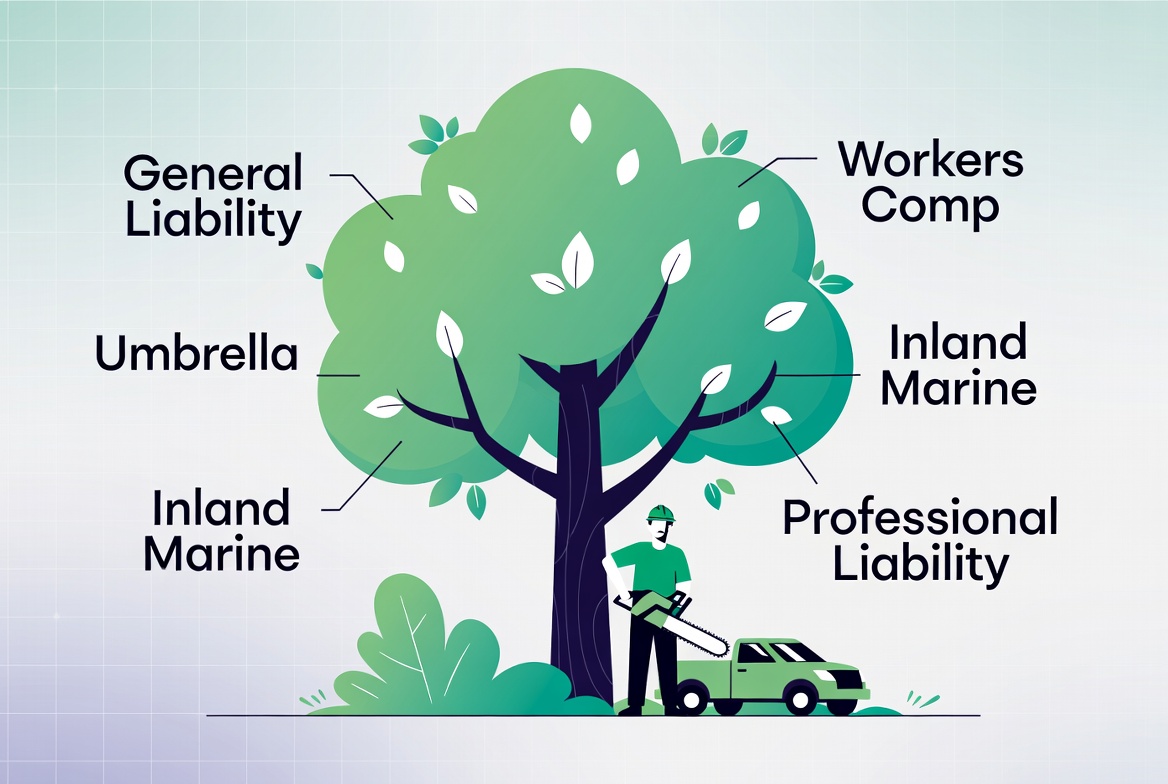

Three Pillars of Tree Service Insurance

Coverage Type

The policy itself — General Liability, Workers Compensation, Commercial Auto, Inland Marine, Umbrella, Excess, Rigging Liability, Crane Coverage, Pollution, Professional Liability, and Hired/Non-Owned Auto.

Operation Type

The kind of tree work being done — removal, trimming, cutting, stump grinding, emergency, storm cleanup, utility line clearance, high-risk removals, residential, commercial, municipal, and forestry contracting.

Buyer & Hard-to-Place

Where you are in the buying process and what makes your account unique — cost, quotes, COIs, requirements, prior claims, post-cancellation placement, declined accounts, crane ops, and accounts without workers comp.

Every Tree & Arborist Page in the Hub

Tree Service Coverage Pages

The individual policies that make up a complete tree service insurance program.

Tree Service Operation Pages

Coverage built around the specific kind of tree work you perform.

Tree Service Insurance Buyer Pages

Pricing, quote requests, certificates of insurance, contract requirements, and onboarding.

Hard-to-Place Tree Service Pages

Solutions for accounts that have been declined, non-renewed, or considered high-risk by standard markets.

Every Tree Account Starts With the Intake Form

Tree work is not light landscaping. Give us the details on climbing, cutting, rigging, equipment, subcontractors, prior claims, and required limits so we can build the right submission.

Climbing crews · Bucket trucks · Cranes · Stump grinders · Subcontractors · Storm work · Utility

Specialty Brokerage Built for High-Severity Risks

Tree-Specific Carrier Relationships

Direct access to specialty markets that underwrite climbing, cranes, rigging, utility clearance, and storm response — the markets standard agencies do not have appointments with.

Hard-to-Place Capability

Prior claims, non-renewals, declinations, gaps in coverage, and accounts coming off assigned-risk pools are placed every week — not turned away.

COI & Additional Insured Speed

Property managers, HOAs, municipal contracts, and large commercial accounts demand specific COI language. We coordinate it at issuance — usually same day after binding.

Subcontractor & Crew Structure Help

1099 climbers, leased crews, crane vendors, and chip-truck subs create exposure most owners do not see. We map the structure and place the right coverage.

Crane & Rigging Expertise

Crane-assisted removals are an underwriting trigger. We have the carriers and the endorsement language to keep them inside the program — not excluded out of it.

Multi-State Placement

Tree contractors traveling for storm work or working across state lines need a broker who can produce filings, COIs, and proper auto coverage in every state on the route.

Coverage That Wraps the Whole Operation

Search the Kelly Insurance Group Site

Other KIG Coverages Tree Contractors Often Add

Tree & Arborist Insurance Questions Answered

What policies make up a complete tree service insurance program?

At minimum: General Liability, Workers Compensation (in most states), and Commercial Auto. Most tree services also need Inland Marine for equipment, an Umbrella for excess limits, and depending on operations — Rigging Liability, Crane Coverage, Pollution Liability, and Hired/Non-Owned Auto. See the GL page, Workers Comp page, and Commercial Auto page.

Why is tree service insurance considered hard to place?

Severity. Roof and vehicle strikes, climbing falls, crane drops, and utility line incidents produce six-figure claims. Standard small-business markets routinely decline tree work. Specialty markets are necessary, which is why we run a dedicated high-risk arborist program.

How much does tree service insurance cost?

It depends on payroll, revenue, equipment, height of work, crane usage, claims history, and required limits. Pricing detail is broken out on our Tree Service Insurance Cost page and Arborist Insurance Cost page.

I had a claim — or got non-renewed. Can you still place me?

Yes. We work with hard-to-place tree accounts every day. Send loss runs and the cancellation notice. Start with the After Cancellation page, the Insurance With Claims page, or the intake form.

Do I need a separate policy for crane-assisted removals?

Crane operations are an underwriting trigger and frequently require specific endorsements, scheduled equipment, and sometimes a separate crane policy. Details on the Crane & Boom Truck page and the Tree Service With Crane Operations page.

Can I get a Certificate of Insurance the same day?

Yes — once your submission is bound, COIs are typically issued same day. Property managers, HOAs, and municipal contracts almost always require additional insured language, which we coordinate at issuance. See the Tree Service COI page.

What about subcontractors and 1099 climbers?

1099 climbers, crane vendors, and chip truck operators create exposures the policyholder is held responsible for under contract. Carriers want to see COIs from subs, hold-harmless agreements, and proper additional insured language. We help map the structure during the submission process.

Where do I start?

Start with the intake form or pick the page closest to your situation from the hub above. If you are not sure where to begin, the General Liability page is the foundation policy and a good first read.

Ready to Place Your Tree Service Account?

Send us climb counts, equipment, subcontractor usage, claims history, and required limits. We build the submission, market it to specialty tree carriers, and get you the policy your contracts demand.

Start the Intake Form → Contact Kelly Insurance Group →