FILM EQUIPMENT INSURANCE

FOR RENTED, OWNED, AND IN-TRANSIT GEAR

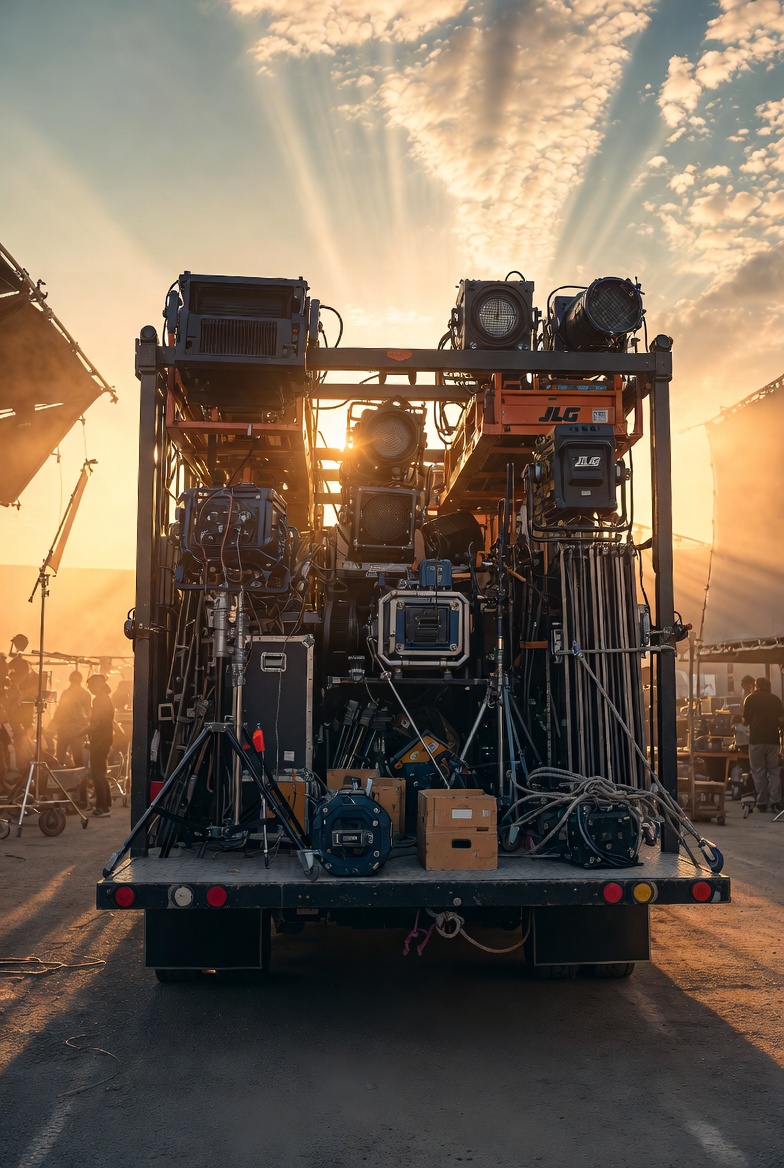

Coverage that satisfies the rental house — and protects the production. Cameras, lenses, lighting, grip, audio, and specialty equipment covered while in your care, custody, and control. Certificates of insurance issued with the additional insured language rental houses actually require.

- RENTED PRODUCTION EQUIPMENT

- OWNED CAMERA & GEAR PACKAGES

- RENTAL HOUSE COIs

- ADDITIONAL INSURED LANGUAGE

- EQUIPMENT IN-TRANSIT

- SPECIALTY & GIMBAL RIGS

- STEADICAM & DRONE PAYLOADS

- CINEMATOGRAPHER OWNED PACKAGES

RENTAL HOUSES WON'T RELEASE GEAR WITHOUT A COI

Equipment coverage is one of the most-required and least-understood lines in a film insurance program. The rental house cares about the COI. The production cares about replacement value. Both need to align.

Film equipment insurance covers the cameras, lenses, lights, grip gear, audio packages, and specialty rigs your production rents or owns — while it's in your care, custody, and control. The phrase "care, custody, and control" matters. It's the legal trigger that determines whether a damaged camera is your problem or someone else's, and it's why generic business insurance often won't satisfy a rental house's COI requirements.

Almost every camera rental house, lighting vendor, grip supplier, and specialty equipment provider in the industry requires a Certificate of Insurance naming them as additional insured before they'll release gear. Many also require specific limit thresholds, scheduled or blanket coverage language, and proof of in-transit coverage if the equipment is moving between locations. We've placed this kind of coverage for productions at every budget tier — from short film shoots through indie features and studio-tier productions.

For projects that need a certificate fast — for a permit deadline, a rental house pickup tomorrow, or a location agreement that needs proof today — equipment coverage is one of the most common rush-issue scenarios we handle.

EVERY CATEGORY OF FILM GEAR

Production equipment isn't one schedule — it's many. Each category has its own carrier appetite, valuation method, and rental house requirements.

CAMERA BODIES

Cinema camera systems including digital and film bodies. Typically the highest-value items on the schedule and the focus of rental house COI requirements.

LENSES & GLASS

Cinema primes, zooms, anamorphic lenses, and specialty glass. High individual values and significant exposure when entire kits travel together.

LIGHTING PACKAGES

HMI, LED, tungsten, fluorescent, and balloon lighting kits. Significant value in fixtures, ballasts, lamps, modifiers, and stands.

GRIP EQUIPMENT

Stands, flags, dollies, jibs, sliders, dance floors, and grip trucks fully outfitted. Often rented as a package from grip houses with strict COI rules.

AUDIO & SOUND

Boom mics, lavaliers, mixers, recorders, wireless systems, and IFB packages. Sensitive to in-transit damage and humidity exposure.

CAMERA SUPPORT

Tripods, fluid heads, geared heads, sliders, and follow-focus systems. Often packaged with the camera body in rental house schedules.

STEADICAM & GIMBAL

Steadicam rigs, motorized gimbals, and stabilizer systems. High-value specialty equipment frequently rented with operator services.

DRONE & AERIAL RIGS

Cinema drones with camera payloads, aerial mounts, and gyroscopic platforms. Specialty coverage often coordinated with separate drone and aerial filming insurance.

SPECIALTY RIGS

Underwater housings, vehicle mounts, motion-control systems, helicopter mounts, and one-off specialty fabrications.

DIFFERENT EQUIPMENT, DIFFERENT POLICIES

How the equipment is owned changes what coverage you actually need. Two structures, two underwriting approaches.

RENTED EQUIPMENT

Coverage for equipment rented from camera houses, lighting vendors, grip suppliers, and specialty providers — while in your care, custody, and control during the production.

- Per-project or short-term coverage windows

- Rental house listed as additional insured

- Specific limit and language requirements per vendor

- Coverage typically based on equipment schedule values

- In-transit coverage often required

OWNED EQUIPMENT

Coverage for cameras, lenses, lighting, and gear owned by the cinematographer, production company, or owner-operator. Usually structured as an annual policy following the equipment wherever it travels.

- Annual policy structure

- Worldwide territory options

- In-transit and on-location coverage

- Scheduled equipment with agreed values

- Coverage available for owner-operator hire scenarios

WHAT'S INSIDE THE COVERAGE

Equipment coverage is more than just "if it breaks, we pay." Here are the structural components that come up most often in film equipment policies.

PHYSICAL DAMAGE

Coverage for direct physical damage to equipment from accidents, drops, water, dust, and other on-set hazards.

THEFT

Equipment stolen from set, vehicles, hotel rooms, and storage. Usually subject to specific loss-control and security requirements.

IN-TRANSIT COVERAGE

Coverage while equipment is being transported between locations, in vehicles, or in transit between rental house and set.

EQUIPMENT IN VEHICLES

Specific coverage for gear in production vehicles — including grip trucks, picture cars, and crew personal vehicles being used for production.

ADDITIONAL INSURED

Extending coverage to name rental houses, equipment owners, and vendors as additional insureds — typically required on every COI.

REPLACEMENT VALUE

Coverage written on a replacement-cost basis rather than depreciated value — important for high-value cinema equipment.

RENTAL REIMBURSEMENT

Coverage for the cost of renting replacement equipment while the damaged item is being repaired or replaced — keeps production running.

WORLDWIDE TERRITORY

Coverage extension for international shoots, including foreign location filming and overseas rental house arrangements.

CERTIFICATE OF INSURANCE REQUIREMENTS

Rental house COI requirements are common across the industry — though specifics vary by vendor. Here are the elements that come up most consistently when picking up gear.

ADDITIONAL INSURED

The rental house listed as additional insured on the COI — typically with their full legal entity name and address.

LOSS PAYEE

Rental house listed as loss payee — meaning insurance proceeds for damaged equipment go directly to them rather than the production.

EQUIPMENT LIMIT

Coverage limits that match or exceed the total replacement value of the rented equipment package being released.

DESCRIPTION OF OPERATIONS

Specific reference to the production, project name, or rental period in the description block of the COI.

WAIVER OF SUBROGATION

Endorsement waiving the carrier's right to seek recovery from the rental house — frequently required by larger vendors.

PRIMARY & NON-CONTRIBUTORY

Endorsement specifying that your policy responds first, ahead of any other coverage the rental house may carry.

COVERAGE TERRITORY

Confirmation of geographic coverage matching the production locations — particularly relevant for productions traveling out of state or internationally.

EFFECTIVE DATE RANGE

Coverage effective dates that span the entire pickup-through-return window — including any prep, shoot, and wrap days.

Specific requirements vary by rental house. We work directly with the vendor's COI checklist when issuing the certificate.

EVERY COMMON EQUIPMENT SITUATION

-

1

RENTING FROM A CAMERA HOUSE

Rental house COI with additional insured, loss payee, and limits matching the package value. Common pickup deadline scenarios handled.

-

2

OWNER-OPERATOR HIRED ON A PRODUCTION

Cinematographer, gaffer, or owner-operator hiring out their owned equipment package for a production — annual coverage following the gear.

-

3

SHOOTING IN MULTIPLE STATES

Equipment traveling between locations and across state lines — coverage that follows the gear including in-transit periods.

-

4

INTERNATIONAL FILMING

Productions shooting overseas with equipment crossing borders. Worldwide territory coverage and customs documentation considerations.

-

5

SAME-DAY COI FOR PICKUP

Tomorrow's pickup with the rental house language they require — common scenario handled through same-day certificate processing.

-

6

SPECIALTY EQUIPMENT

Drones, underwater housings, vehicle mounts, motion control rigs — coverage placed for specialty rigs that generalist policies decline.

-

7

EQUIPMENT IN VEHICLES OVERNIGHT

Loss-control and theft coverage for equipment stored in production vehicles, hotel rooms, and on-location overnight storage.

QUESTIONS FROM PRODUCERS, DPs & RENTAL HOUSES

WHAT DOES FILM EQUIPMENT INSURANCE COVER?

DO I NEED INSURANCE TO RENT FROM A CAMERA HOUSE?

HOW DO I GET A CERTIFICATE OF INSURANCE FOR THE RENTAL HOUSE?

HOW MUCH DOES FILM EQUIPMENT INSURANCE COST?

DOES PRODUCTION INSURANCE INCLUDE EQUIPMENT COVERAGE?

WHAT IS CARE, CUSTODY, AND CONTROL?

WHAT IF I OWN MY OWN CAMERA PACKAGE?

DOES EQUIPMENT INSURANCE COVER DRONES?

RENTAL HOUSE NEEDS A COI. YOU NEED A BROKER WHO MOVES.

Whether you're picking up a camera package tomorrow, hiring out your owned cinema rig, or building a multi-location production with traveling equipment — we structure equipment coverage that satisfies the rental house and protects the production.

THE COMPLETE FEATURE FILM INSURANCE LIBRARY

FEATURE FILM INSURANCE

The complete overview of feature film coverage — every spoke, every policy type, every budget tier.