Higher Limits. Cleaner Contracts. Faster Turnaround.

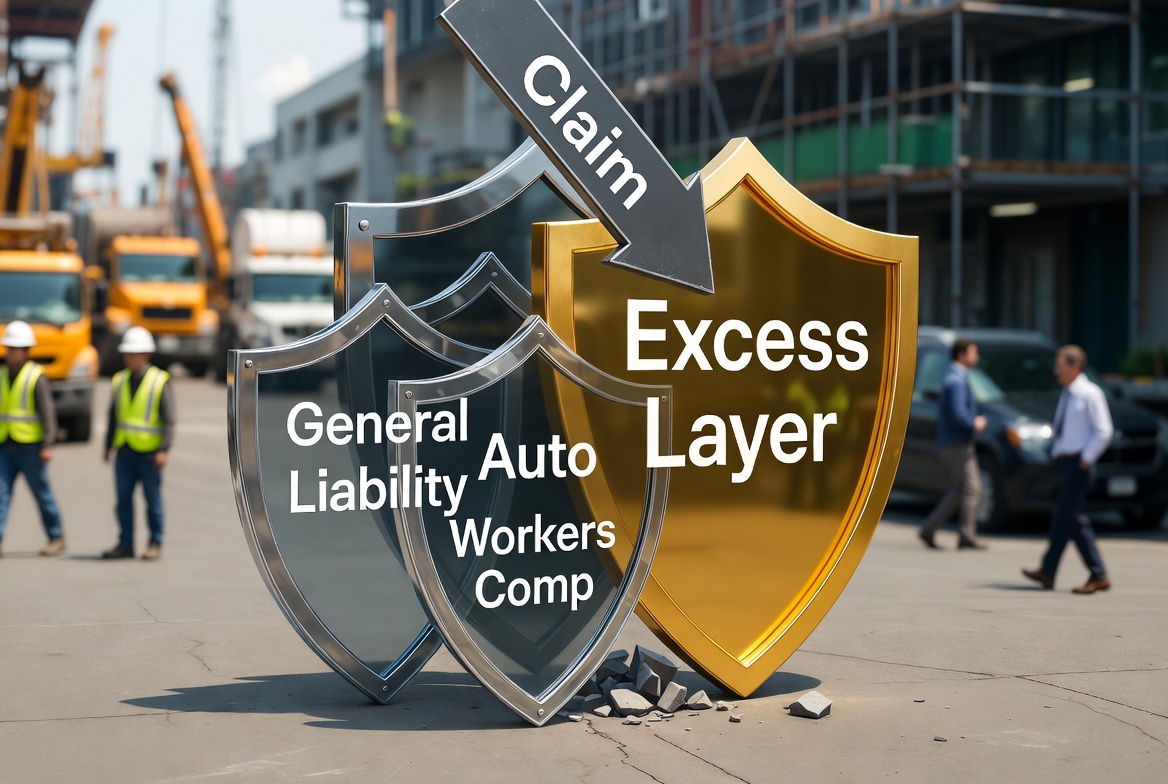

Need higher limits fast? A commercial umbrella — also called commercial excess liability — stacks above your General Liability, Auto, and Employers Liability so one shock loss doesn't cap your growth or break a contract requirement. We place $1M, $2M, $5M, $10M, $20M+, including monoline, follow-form, and layered tower structures.

What An Umbrella / Excess Policy Sits Over.

Most umbrellas are follow-form: if it's excluded below, it's usually excluded above unless endorsed. Here's the typical stack.

Built For Contract Limits

Owners, GCs, venues, and lenders frequently require $5M–$10M+ total limits. We map your contracts to the cleanest structure.

Shock-Loss Cushion

Large bodily-injury, property-damage, or auto losses can exhaust primary limits in one claim. Umbrella is the buffer.

Monoline Or Attached

Stand-alone umbrella, follow-form excess, or a layered tower with multiple carriers — we structure all three.

AI / Primary & Non-Contributory

We endorse additional insureds, waivers of subrogation, and primary/non-contributory wording to match contracts exactly.

Pricing Basics.

Carriers price umbrella based on class of business, payroll/sales, fleet size, loss history, and underlying limits. The tool below is illustrative only — not a quote.

Very rough illustration (not a quote). Actual pricing depends on class of business, auto exposure, underlying schedule, and loss history.

What Drives Your Premium.

Class of business. A real-estate LLC and a heavy-haul trucking company will price 10x apart at the same limit. Class is the single biggest input.

Auto exposure. Vehicle counts, GVWR, radius of operation, driver MVRs, and accident frequency move umbrella pricing more than any other factor.

Underlying schedule. Higher underlying GL and auto limits (e.g., $2M GL vs $1M GL) often reduce the umbrella rate per million.

Loss history. 5 years of clean loss runs is the strongest leverage you have. Open severity claims will raise rate or attach point.

Contract requirements. If the contract demands $10M but you only need $5M operationally — we'll help you weigh the cost vs the deal value.

Download Supplement (PDF)Who Buys Umbrella & Excess From KIG.

Some classes practically live and die on umbrella. Here's the shortlist.

Contractors

GCs, subs, roofers, riggers, welders — most prime contracts demand $5M–$10M+ excess.

Trucking / Fleets

Auto severity is the #1 umbrella driver. Owner-ops to large fleets — we shop the tower.

Real Estate / Apartments

Apartment owners, multi-property LLCs, condo associations — habitational and slip-and-fall risk.

Crane & Rigging

Severity is everything. $10M–$25M limits standard. We layer with monoline excess as needed.

Events & Entertainment

Concerts, festivals, venues, productions. Most venue contracts demand $5M+ in additional excess.

LLCs / Holding Cos

Single-purpose LLCs and operating companies stacked under a parent. We map the structure.

Commercial Umbrella & Excess Topics.

Explore pricing, higher limits, exclusions, contract requirements, industry-specific umbrella needs, and excess liability structure.

How Much Does Commercial Umbrella Insurance Cost?

Read Higher Limits$10 Million Umbrella Liability Insurance

Read Large Programs$20 Million Commercial Excess Liability Program

Read ComparisonUmbrella vs. Excess Liability Insurance

Read CoverageWhat Commercial Umbrella Insurance Covers

Read ExclusionsWhat Commercial Umbrella Does Not Cover

Read ContractsContract Umbrella Insurance Requirements

Read AI / PNCAdditional Insured, Primary & Non-Contributory

Read Policy StructureFollow Form vs. Monoline Umbrella

Read Layered TowersHow $10M+ Excess Towers Are Built

Read ContractorsContractor Umbrella & Excess Liability

Read Crane & RiggingCrane & Rigging Umbrella Liability

Read TruckingTrucking Umbrella & Excess For Fleets

Read EventsEvent & Entertainment Umbrella Liability

Read Hard To PlaceDeclined Or Non-Renewed Umbrella

Read Excess OnlyExcess Liability For Businesses

ReadCommercial Umbrella & Excess FAQ.

How Much Is A $1M Commercial Umbrella?

It varies by class, auto exposure, payroll/sales, underlying terms, and loss history. Many low-hazard businesses can start in the low four figures annually. Heavy auto, contractors, and habitational risks price higher.

How Much Is A $5M Umbrella?

Often mid-four to five figures annually depending on class, auto exposure, underlying limits, and loss history. Many programs at $5M+ are built in layers with multiple carriers.

What Does Umbrella Sit Over?

Typically General Liability, Commercial Auto, and Employers Liability. Some carriers allow additional underlying schedules — professional liability, garage liability, or liquor liability — depending on class and form.

What Does A Commercial Umbrella NOT Cover?

Umbrella generally follows form. If it's excluded on the underlying, it's usually excluded above unless specifically endorsed. Common exclusions: pollution, professional services, cyber, employment practices, owned property. Details vary by carrier.

What's The Difference Between Umbrella And Excess?

"Excess" strictly follows form — same coverage as underlying, just more limit. "Umbrella" can sometimes broaden coverage by dropping down for gaps in the underlying or covering claims the underlying doesn't. The terms get used interchangeably, but the form wording matters.

Do I Need $10M Or $20M+?

If contracts, venues, owners, or lenders require higher total limits, or your exposure includes higher-severity risks (heavy auto, crowds, foot traffic, large portfolios) — yes. Higher limits are often a cost-efficient balance-sheet protector.

I Was Declined. Can You Still Place Excess For Me?

Yes. Non-renewal and decline are common reasons to come to KIG. We work with surplus and specialty carriers that will quote roofers, demo crews, fleets with claims, and other hard-to-place classes.

What's A Layered Tower?

For limits over $10M, one carrier rarely writes the full amount. We stack multiple carriers — e.g., $5M primary excess + $5M first layer + $10M second layer — to build a $20M tower. We negotiate the structure across markets.

Request Umbrella Options

Send your underlying dec pages and loss runs separately and we'll move fast. Or just call/text (412) 212-2800.

More Resources Across Our Programs.

Pollution, action-over, school programs, aviation, and the underlying lines that umbrella sits on top of.

Underlying Lines & Programs

Pollution & Environmental

Action Over & NY Labor Law

Management & Specialty Lines

Aviation & School Programs

Call or text anytime — even in the middle of the night. If we're able to answer, we will.

📞 Call / Text (412) 212-2800