LIFE INSURANCE FOR BLENDED FAMILIES

Kelly Insurance Group helps blended families navigate the complexity of life insurance planning across prior relationships, court-ordered obligations, and new household structures — ensuring every child in the family is financially protected and every coverage obligation from prior marriages is being met.

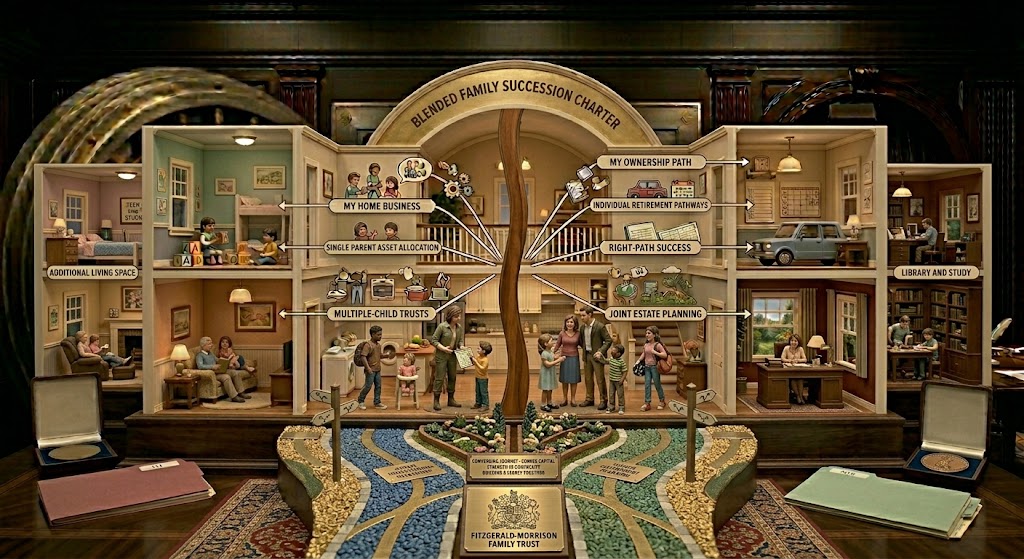

SELECT YOUR BLENDED FAMILY SITUATION TO SEE THE COVERAGE PLANNING CONSIDERATIONS.

Each spouse needs individual life insurance sized to support their biological children regardless of what happens in the new marriage. Coverage must account for existing child support obligations, any court-ordered life insurance from prior divorce decrees, and the new household's shared financial obligations. Beneficiary designations must be carefully structured — a surviving spouse named as primary beneficiary may not distribute proceeds to the deceased spouse's biological children as intended.

DISCUSS YOUR BLENDED FAMILY COVERAGE WITH KELLY INSURANCE GROUPThe stepparent may have no legal obligation to support their stepchildren — but the biological parent's death creates a real financial need for those children regardless of the stepparent's relationship. Life insurance on the biological parent must be sized to support those children independently. The stepparent's coverage need reflects the shared household obligations and any biological children of their own.

DISCUSS YOUR BLENDED FAMILY COVERAGE WITH KELLY INSURANCE GROUPChildren from the current relationship and children from prior relationships may have very different financial protections if the parents die. A comprehensive coverage plan addresses each child's needs explicitly — not through a single death benefit that may be allocated in ways that leave some children underprotected. Trust structures and specific beneficiary designations provide the most reliable protection for all children.

DISCUSS YOUR BLENDED FAMILY COVERAGE WITH KELLY INSURANCE GROUPA prior divorce decree may require maintaining specific coverage for an ex-spouse or biological children. These obligations do not disappear in a new marriage. Confirm the existing court-ordered requirements, ensure the coverage is in place, and review how the new household's coverage program interacts with the prior obligations. Noncompliance with court-ordered coverage is a legal exposure, not just a planning gap.

DISCUSS YOUR BLENDED FAMILY COVERAGE WITH KELLY INSURANCE GROUP

WHY BLENDED FAMILY LIFE INSURANCE REQUIRES MORE INTENTIONAL PLANNING THAN A STANDARD HOUSEHOLD.

A SINGLE DEATH BENEFIT PAID TO A SURVIVING SPOUSE MAY NOT PROTECT ALL CHILDREN

In a blended family, a death benefit paid to the surviving spouse does not guarantee that the deceased spouse's biological children from a prior relationship will receive the financial support intended. The surviving spouse controls the funds and has no legal obligation to distribute them to stepchildren. Trust structures — with specific distribution instructions for each set of children — provide the protection that a straightforward beneficiary designation cannot.

PRIOR DIVORCE DECREES CREATE LIFE INSURANCE OBLIGATIONS THAT MUST BE MAINTAINED

A divorce decree that requires life insurance for the benefit of an ex-spouse or biological children remains legally enforceable in the new marriage. The new household's coverage program must account for these existing obligations — they are not optional and they do not expire when a new marriage begins. Review every prior divorce decree for insurance provisions before restructuring coverage.

BENEFICIARY DESIGNATIONS IN A BLENDED FAMILY REQUIRE LEGAL GUIDANCE

The interaction between a will, a trust, a beneficiary designation, and a prior divorce decree can create unintended outcomes in a blended family situation. A life insurance policy with a simple individual beneficiary designation may produce results that conflict with the estate plan, the divorce decree, and the insured's actual intent. Trust structures and estate planning attorney review are worth the investment in a blended family context.

EXPLORE MORE FAMILY LIFE INSURANCE RESOURCES

FREQUENTLY ASKED QUESTIONS.

Can I name my current spouse as beneficiary if I have children from a prior marriage?

You can, but it may not protect your biological children from the prior relationship. A spouse who receives the death benefit has no legal obligation to use those funds for the benefit of your biological children. A trust as beneficiary — with specific distribution instructions for your biological children — provides the protection that a direct spousal designation does not.

Does a new marriage change my court-ordered life insurance obligations from a prior divorce?

No. Court-ordered life insurance obligations from a prior divorce decree remain in effect regardless of a new marriage. You must maintain the required coverage, in the required amount, with the required beneficiary, for the duration specified in the decree. Non-compliance is contempt of court and exposes you to legal consequences that affect your entire current household.

What is the best beneficiary structure for a blended family?

There is no single correct structure — it depends on the specific family composition, prior divorce decree requirements, and estate planning objectives. Common approaches include a trust as beneficiary with specific distribution allocations for each set of children, irrevocable beneficiary designations as required by prior decrees, and separate policies on each spouse sized to their respective children's needs. An estate planning attorney should review and coordinate the complete structure.

Does life insurance for a stepparent need to cover stepchildren?

A stepparent has no legal obligation to support stepchildren, but may choose to include them in coverage planning. More importantly, the biological parent's life insurance must be sized and structured to support their biological children independently — without relying on the stepparent to fill the gap. The stepparent's coverage should address their own biological children and the shared household obligations.

How should we handle life insurance if we have children together in addition to prior children?

Each set of children — from the current relationship and from prior relationships — should have explicitly addressed financial protection. A single death benefit paid to the surviving spouse may provide for the current relationship's children but leave prior children unprotected. Separate policies, trust structures with specific distribution instructions, or explicit beneficiary designations that allocate portions to each set of children are all approaches worth considering with an estate planning attorney.

What happens to my children from a prior marriage if I die and my current spouse remarries?

Your children's financial protection should not depend on your surviving spouse's future decisions — including the decision to remarry. A trust as beneficiary of your life insurance, with distribution instructions that provide for your biological children over time, ensures their financial security regardless of what your surviving spouse does after your death.

READY TO GET STARTED?

MAKE SURE EVERY CHILD IN YOUR BLENDED FAMILY IS FINANCIALLY PROTECTED.

Kelly Insurance Group helps blended families build life insurance programs that protect every child — biological and step — while meeting court-ordered obligations from prior relationships and coordinating with the current household's estate plan.

The availability of coverage and eligibility for coverage can depend on numerous factors. We cannot guarantee that all customers, individuals, and businesses looking for coverage will be successful in these efforts when contacting our team. All policy coverages and terms need to be fully reviewed by the respective consumer to ensure the coverage asked for is what is specifically being quoted or provided by any insurance policy. Insurance Policies, Coverage Changes, and their terms and conditions are not bound or altered until written confirmation is provided by one of our licensed team members or underwriters. This page does not offer legal advice, legal opinions, or policy interpretations. Rather, this page is meant as a resource to help provide customers and insurance consumers with additional considerations that may help in their insurance buying or pursuit of insurance information. Kelly Insurance Group does not employ or direct attorneys.