Semiconductor & Advanced Manufacturing Insurance

Semiconductor and advanced manufacturing operations create a different insurance environment than ordinary manufacturing businesses. These companies may involve clean-room production, robotics integration, wafer fabrication, mission-critical process control, microelectronics, lithium battery manufacturing, contamination-sensitive production, imported machinery, expensive automation systems, utility dependency, cyber-physical controls, and strict customer-driven insurance requirements. Kelly Insurance Group works with complex commercial insurance placements where the underwriting story, production environment, equipment values, operational dependency, and contractual obligations matter.

Insurance for Semiconductor Facilities, Clean-Room Contractors, Robotics Integrators, and Advanced Manufacturing Companies

Semiconductor and advanced manufacturing operations often depend on precise production tolerances, contamination control, expensive equipment, uptime stability, and interconnected automation systems. A relatively small issue can become a major operational event if production lines stop, robotics systems fail, contamination spreads, utility interruption occurs, or a critical component delays customer delivery schedules.

Standard manufacturing applications usually fail to explain these businesses correctly. “Manufacturer” does not explain whether the company fabricates wafers, integrates robotics, installs semiconductor equipment, operates a clean room, manufactures microelectronics, supports mission-critical facilities, or develops automation systems connected to industrial controls.

Kelly Insurance Group focuses on difficult commercial insurance placements where the insurance structure needs to match the actual production environment. Semiconductor and advanced manufacturing accounts often require careful explanation of operational dependency, contamination exposure, production bottlenecks, customer concentration, business interruption severity, cyber-physical systems, products exposure, and contractual insurance obligations.

Advanced Manufacturing Insurance Commonly Involves

- High-value fabrication equipment, robotics, production systems, and specialized machinery

- Clean-room contamination sensitivity and environmental control systems

- Business interruption, utility dependency, and production downtime exposure

- Products liability and downstream component failure concerns

- Technology E&O, robotics integration, software, and controls exposure

- Cyber liability tied to operational technology and connected production systems

- Contract-driven insurance requirements from OEMs and large customers

- Imported equipment, inland marine, cargo, and transit exposure

- Workers compensation exposure tied to technical production environments

- Excess liability driven by severity and contract requirements

Semiconductor & Advanced Manufacturing Risk Environment

Semiconductor and advanced manufacturing operations frequently involve a combination of high-value property, automation dependency, contamination-sensitive production, expensive downtime exposure, and strict customer expectations. These operations may rely on robotics, industrial automation, mission-critical controls, clean-room environments, precision handling, advanced testing, and specialized process equipment.

Who This Insurance Hub Is Built For

This page is designed for semiconductor facilities, robotics companies, advanced manufacturing firms, automation integrators, clean-room contractors, microelectronics manufacturers, mission-critical production environments, and related technical operations that require more than a basic manufacturing insurance approach.

Semiconductor & Advanced Manufacturing Specialization Blocks

These supporting sections are intentionally built into the hub page for now so the content is indexable, useful, and substantial without creating thin standalone pages prematurely.

Semiconductor Fabrication Plant Insurance

Semiconductor fabrication facilities create one of the most demanding insurance environments in commercial manufacturing. These facilities may depend on clean rooms, environmental stability, specialized utility systems, process gases, robotics, expensive production tools, contamination controls, water systems, and mission-critical HVAC infrastructure.

The physical property value is only part of the issue. Downtime severity can become the dominant exposure if production interruption delays customer contracts, disrupts semiconductor supply chains, or prevents the operation from maintaining production commitments.

Semiconductor Facilities Require More Detailed Underwriting

Fabrication facilities often need more explanation than a normal manufacturing account because underwriters need to understand contamination controls, backup systems, production bottlenecks, utility dependency, process sensitivity, fire protection, equipment breakdown exposure, and operational recovery planning.

Common Review Areas

- Production equipment values and dependency

- Business interruption and extra expense exposure

- Utility interruption concerns

- Contamination controls and environmental stability

- Fire protection systems and suppression infrastructure

- Supply chain dependency and customer concentration

Clean Room Contractor Insurance

Clean-room contractors may design, install, maintain, validate, clean, modify, or support controlled production environments used in semiconductor, medical device, aerospace, battery, biotechnology, and electronics manufacturing operations.

The insurance structure depends heavily on what the contractor actually performs. A company cleaning clean rooms creates a different risk profile than a contractor designing and commissioning a semiconductor production environment.

Contamination Exposure Changes the Insurance Conversation

If the contractor’s work can affect contamination integrity, sterility, production stability, or environmental controls, the insurance structure usually requires more careful review involving general liability, professional liability, contractor pollution liability, and installation-related exposures.

Important Underwriting Questions

- Does the contractor design or install the environment?

- What industries are served?

- Are contamination-sensitive environments involved?

- Does the contract require E&O or pollution liability?

- Are subcontractors involved?

- Does work occur in active production environments?

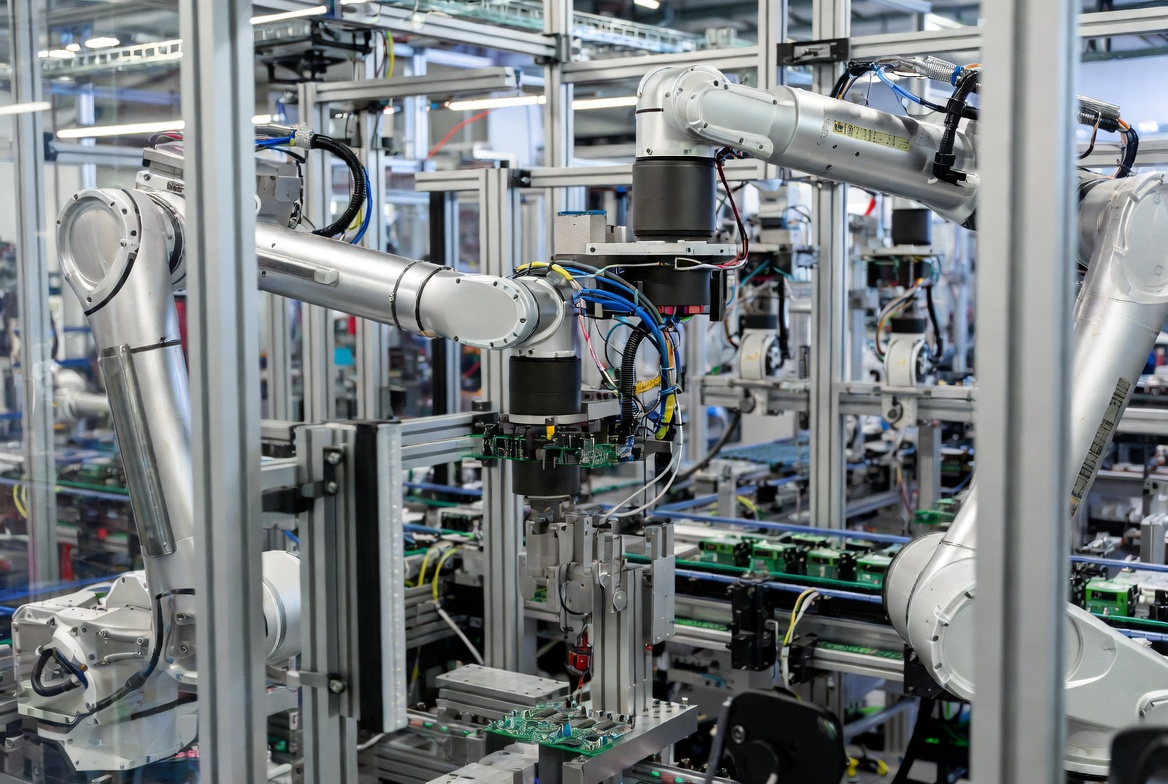

Precision Robotics Integrator Insurance

Robotics integrators combine programming, electrical systems, controls, sensors, safety systems, machine vision, installation, commissioning, and production-line integration. These businesses frequently operate between contractor, software vendor, engineering consultant, and manufacturer.

That hybrid role creates blended exposure involving bodily injury, production interruption, products liability, software failure, system performance, cyber exposure, and completed operations liability.

Robotics Integration Creates Cyber-Physical Exposure

A robotics system failure may involve software, physical motion, controls, guarding, production interruption, bodily injury, or damage to customer property. Insurance review should evaluate what is programmed, what is installed, and what performance responsibility exists.

Coverage Areas Often Reviewed

- General liability and completed operations

- Products liability exposure

- Technology E&O and software responsibility

- Cyber liability involving connected systems

- Contractual performance obligations

- Machine safety and guarding procedures

Semiconductor & Advanced Manufacturing Coverage Structure

Semiconductor and advanced manufacturing operations often require coordinated coverage structures rather than a single policy approach. The correct structure depends on property exposure, production dependency, customer contracts, contamination sensitivity, automation systems, product exposure, and operational complexity.

What Underwriters Need to Understand

Semiconductor and advanced manufacturing submissions usually require significantly more detail than ordinary manufacturing accounts. Underwriters often need to understand production dependency, process sensitivity, contamination controls, customer industries, cyber-physical exposure, contractual obligations, and the actual operational role of the business.

| Issue | Why It Matters | Helpful Information |

|---|---|---|

| Actual Operation | Different advanced manufacturing operations create very different insurance environments. | Detailed operational descriptions and service breakdowns. |

| Equipment Dependency | High-value machinery and production tools can create severe interruption exposure. | Machinery schedules, dependency analysis, and equipment values. |

| Business Interruption | Downtime may become financially severe even with limited physical damage. | Business income worksheets and recovery planning information. |

| Products Exposure | Advanced components used in critical systems can create greater severity. | End-use industries and customer concentration details. |

| Cyber & Automation | Connected systems create operational technology and cyber exposure. | Cyber controls, remote access controls, and backup procedures. |

| Contracts | OEMs and large customers may impose strict insurance requirements. | Insurance sections of contracts and vendor requirements. |

Customer Contracts Frequently Drive the Insurance Structure

Semiconductor and advanced manufacturing companies frequently discover that the real insurance issue exists inside customer contracts, OEM agreements, vendor onboarding requirements, lender requirements, or project specifications.

A business may already carry insurance, but contracts may require additional insured wording, waiver of subrogation, primary and non-contributory language, cyber liability, technology E&O, products liability, pollution liability, or excess liability limits that exceed the current structure.

Insurance requirements should be reviewed before production deadlines or onboarding deadlines become urgent. A certificate of insurance cannot create coverage that does not actually exist within the policy structure.

Information That Helps The Quoting Process

- Detailed operational description

- Current policies and loss history

- Customer contract insurance requirements

- Equipment schedules and property values

- Business interruption estimates

- Cyber and operational technology details

- Products manufactured and end-use industries

- Clean-room or contamination-sensitive exposure

- Automation and robotics responsibilities

- Quality-control and testing procedures

FIND RELATED COVERAGE FAST

Search by industry, coverage type, contract requirement, or hard-to-place exposure.

Semiconductor & Advanced Manufacturing Insurance FAQs

What makes semiconductor insurance different from ordinary manufacturing insurance?

Semiconductor operations often involve contamination-sensitive environments, expensive machinery, mission-critical production, utility dependency, and severe downtime exposure that create a more complex insurance environment than standard manufacturing.

Do robotics integrators need technology E&O?

Robotics and automation companies may need technology E&O or professional liability review when they perform programming, controls integration, system design, automation engineering, or performance-sensitive work.

Why is business interruption important for advanced manufacturing?

Advanced manufacturing operations may rely on expensive equipment, environmental stability, utility dependency, production bottlenecks, and strict customer delivery schedules. A relatively small event can disrupt operations significantly.

Can contracts affect the insurance structure?

Customer contracts, OEM agreements, and vendor onboarding requirements frequently drive insurance requirements involving limits, cyber liability, E&O, additional insured wording, waiver of subrogation, and excess liability.

Have a Semiconductor, Robotics, or Advanced Manufacturing Risk?

Semiconductor and advanced manufacturing insurance requires more than a generic manufacturing application. The underwriting conversation often depends on contamination controls, production dependency, equipment values, automation systems, contracts, products exposure, cyber-physical integration, and operational severity. Kelly Insurance Group works with difficult commercial insurance placements involving technical production environments and complex operational risk.